Enabling everyday transactions without relying on UPI

Enabling everyday transactions without relying on UPI

Enabling everyday transactions without relying on UPI

Introduced e₹ without interrupting how people already send, receive, or think about money.

Introduced e₹ without interrupting how people already send, receive, or think about money.

Introduced e₹ without interrupting how people already send, receive, or think about money.

Investment

Investment

Investment

Mobile banking

Mobile banking

Mobile banking

Project overview

Project overview

In 2023, the RBI introduced the Digital Rupee (e₹), which is India’s official Central Bank Digital Currency (CBDC). At first, the RBI launched its own app for testing, but the plan is to bring e₹ into regular banking and fintech apps.

To support this shift, RBI is asking banks to not just add e₹ as a feature but also create simple and user-friendly experiences. The aim is to help people understand and start using e₹ just like they use UPI today.

In 2023, the RBI introduced the Digital Rupee (e₹), which is India’s official Central Bank Digital Currency (CBDC). At first, the RBI launched its own app for testing, but the plan is to bring e₹ into regular banking and fintech apps.

To support this shift, RBI is asking banks to not just add e₹ as a feature but also create simple and user-friendly experiences. The aim is to help people understand and start using e₹ just like they use UPI today.

My Role

My Role

• UI/UX Designer

• Interaction Designer

• UI/UX Designer

• Interaction Designer

Other team members

Other team members

UI/UX Designer

Product Managers

Developers

UI/UX Designer

Product Managers

Developers

Timeline

Timeline

1 month

1 month

Problem statement

Problem statement

Even though the Digital Rupee was launched by the RBI, most users still don’t understand what it is or why they should use it. People are already comfortable with UPI, which is fast, familiar, and works well for everyday payments.

Even though the Digital Rupee was launched by the RBI, most users still don’t understand what it is or why they should use it. People are already comfortable with UPI, which is fast, familiar, and works well for everyday payments.

Objectives

Objectives

Our challenge at Kotak was to design an experience that:

Our challenge at Kotak was to design an experience that:

Our challenge at Kotak was to design an experience that:

Introduces CBDC in a simple and trustworthy way

Introduces CBDC in a simple and trustworthy way

Introduces CBDC in a simple and trustworthy way

Feels familiar, even though it works differently from UPI

Feels familiar, even though it works differently from UPI

Feels familiar, even though it works differently from UPI

Handles wallet-based limitations like balance caps

Handles wallet-based limitations like balance caps

Handles wallet-based limitations like balance caps

Guides users through a new payment flow without overwhelming them

Guides users through a new payment flow without overwhelming them

Guides users through a new payment flow without overwhelming them

Encourages adoption while maintaining regulatory compliance

Encourages adoption while maintaining regulatory compliance

Encourages adoption while maintaining regulatory compliance

Handles wallet-based limitations like balance caps

Handles wallet-based limitations like balance caps

Handles wallet-based limitations like balance caps

Target audience

Target audience

The immediate focus was on people who were already using digital payments, especially UPI, for everyday transactions. These users are generally comfortable with mobile apps.

The immediate focus was on people who were already using digital payments, especially UPI, for everyday transactions. These users are generally comfortable with mobile apps.

The audience included:

The audience included:

Urban and semi-urban users who use UPI regularly for P2P and merchant payments

Working professionals who are familiar with mobile banking

Retail merchants and small business owners who accept QR-based payments

Early adopters curious about new features like offline transactions and digital wallets

Urban and semi-urban users who use UPI regularly for P2P and merchant payments

Working professionals who are familiar with mobile banking

Retail merchants and small business owners who accept QR-based payments

Early adopters curious about new features like offline transactions and digital wallets

What is CBDC?

What is CBDC?

CBDC stands for Central Bank Digital Currency.

It is a digital version of cash, issued and backed by the Reserve Bank of India (RBI).

CBDC stands for Central Bank Digital Currency.

It is a digital version of cash, issued and backed by the Reserve Bank of India (RBI).

Think of it as:

Think of it as:

Digital cash you can keep in a wallet app, even if you don’t have a bank account.

Unlike UPI, which transfers money between bank accounts, CBDC is the money itself, just in digital form. It can be used for:

Unlike UPI, which transfers money between bank accounts, CBDC is the money itself, just in digital form. It can be used for:

Paying someone directly

Buying things at shops

Receiving subsidies or government payments

Even working offline (planned by RBI)

Paying someone directly

Buying things at shops

Receiving subsidies or government payments

Even working offline (planned by RBI)

Circulation value

₹16.4 Cr in Mar 2023 → ₹234 Cr by Mar 2024 → ₹1,016 Cr by Mar 2025 (10× rise)

₹16.4 Cr in Mar 2023 → ₹234 Cr by Mar 2024 → ₹1,016 Cr by Mar 2025 (10× rise)

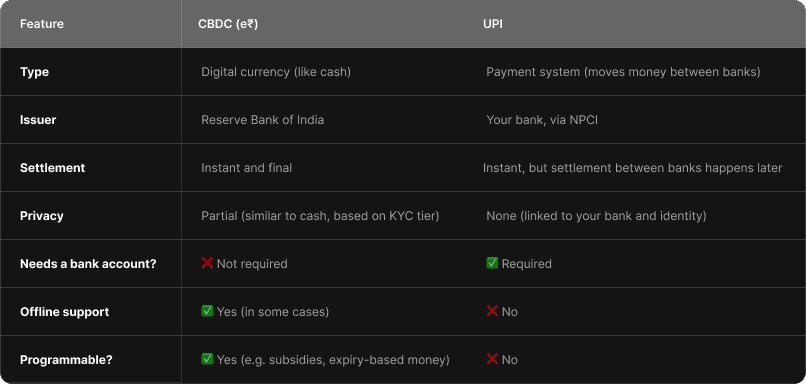

CBDC vs UPI

CBDC vs UPI

UPI moves money. CBDC is the money.

This helps RBI build a parallel digital system that doesn’t depend fully on banks, internet, or third-party apps.

This helps RBI build a parallel digital system that doesn’t depend fully on banks, internet, or third-party apps.

Why RBI is moving toward CBDC?

To reduce dependency on banks for small transactions

To cut physical cash management costs

To enable smart subsidies & offline payments

To offer a better digital alternative to private cryptocurrencies

To build resilient payment infrastructure, beyond UPI

To reduce dependency on banks for small transactions

To cut physical cash management costs

To enable smart subsidies & offline payments

To offer a better digital alternative to private cryptocurrencies

To build resilient payment infrastructure, beyond UPI

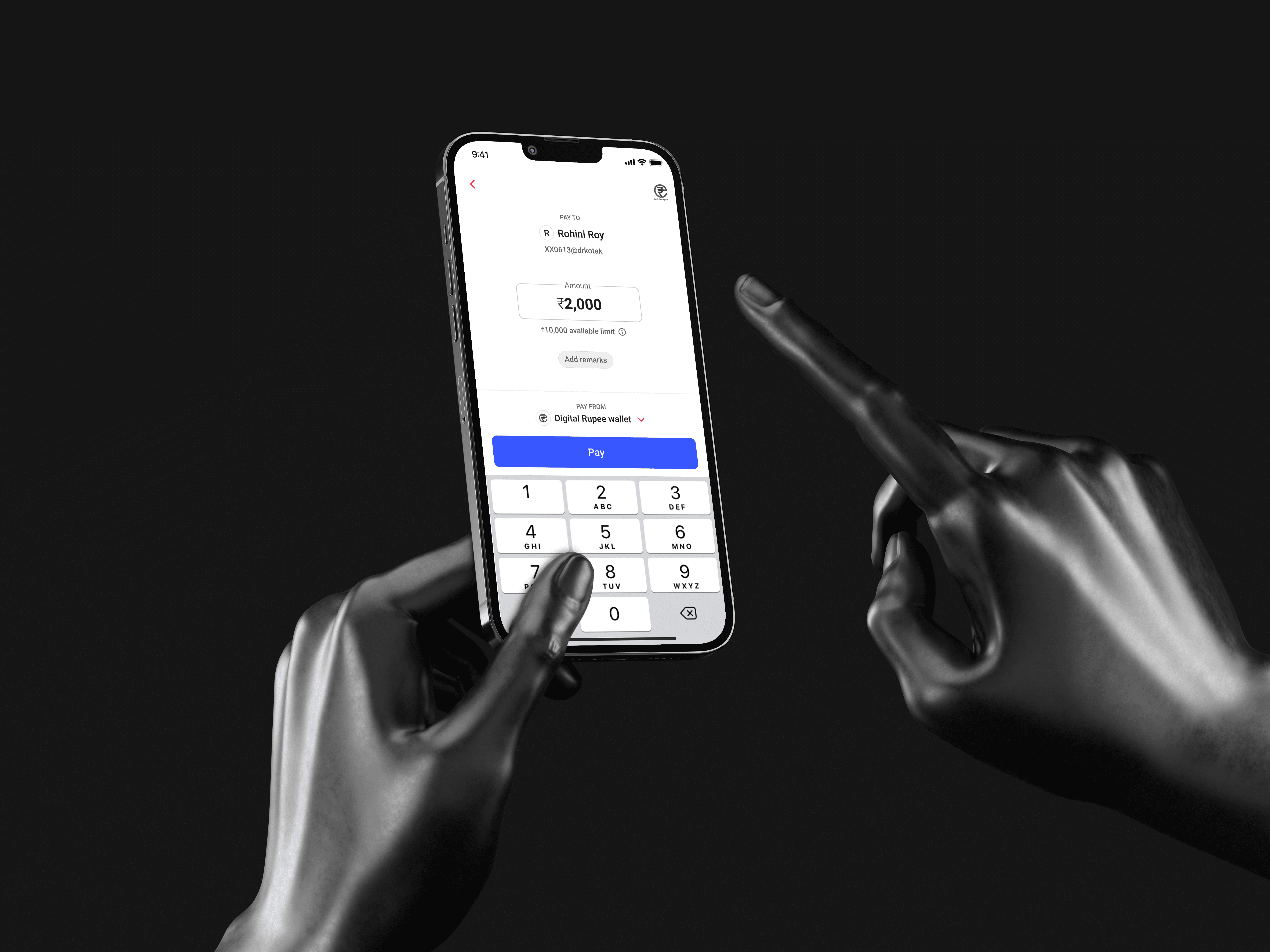

Design approach

Design approach

To keep the experience familiar and reduce learning effort for users, we built the e₹ flow by reusing patterns already present in the Kotak app.

To keep the experience familiar and reduce learning effort for users, we built the e₹ flow by reusing patterns already present in the Kotak app.

We initially treated e₹ like an account, similar to savings or current accounts.

We initially treated e₹ like an account, similar to savings or current accounts.

We used flows like “Add Money”, “Withdraw”, and “Send Money” from our existing designs which were used in some other modules by making modifications as needed.

We used flows like “Add Money”, “Withdraw”, and “Send Money” from our existing designs which were used in some other modules by making modifications as needed.

Later, in some other project which was going parallelly, we decided to create a new "Wallet" section in the app. This section grouped all items you’d find in a physical wallet — debit cards, credit cards, tickets, and cash.

Later, in some other project which was going parallelly, we decided to create a new "Wallet" section in the app. This section grouped all items you’d find in a physical wallet — debit cards, credit cards, tickets, and cash.

To make e₹ feel relatable to physical cash, we placed the e₹ wallet inside this Wallet section as a digital version of cash.

To make e₹ feel relatable to physical cash, we placed the e₹ wallet inside this Wallet section as a digital version of cash.

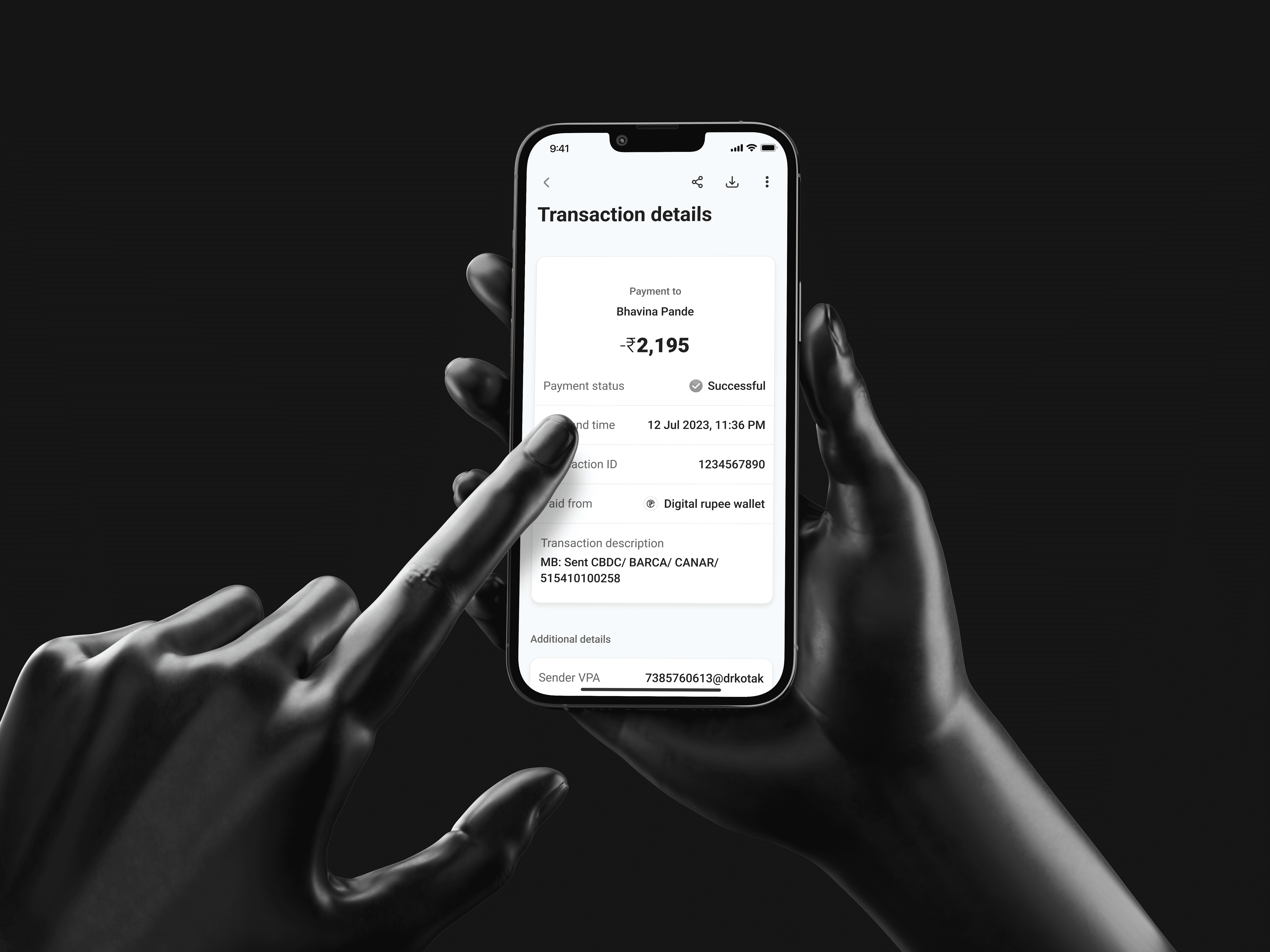

We kept all other flows consistent with the app, only modifying them slightly to support e₹-specific rules like wallet balance, offline status, and transaction syncing.

We kept all other flows consistent with the app, only modifying them slightly to support e₹-specific rules like wallet balance, offline status, and transaction syncing.

This approach helped keep the design cohesive while introducing a completely new payment experience.

This approach helped keep the design cohesive while introducing a completely new payment experience.

Design challenges

Design challenges

We had to make e₹ feel familiar while handling features that were very different from UPI.

We had to make e₹ feel familiar while handling features that were very different from UPI.

We had to make e₹ feel familiar while handling features that were very different from UPI.

Lack of user awareness

Lack of user awareness

Most users didn’t know what e₹ was or how it worked.

No clear reason to switch from UPI

No clear reason to switch from UPI

No clear reason to switch from UPI

Since UPI already works well, users needed a strong reason or benefit to try this.

Since UPI already works well, users needed a strong reason or benefit to try this.

Since UPI already works well, users needed a strong reason or benefit to try this.

Wallet-based flow was unfamiliar

Wallet-based flow was unfamiliar

Wallet-based flow was unfamiliar

Users had to load money into a separate e₹ wallet, which added an extra step.

Users had to load money into a separate e₹ wallet, which added an extra step.

Users had to load money into a separate e₹ wallet, which added an extra step.

Maintaining familiarity while introducing something new

Maintaining familiarity while introducing something new

The design needed to feel close to UPI in terms of flow and interactions, but still handle new CBDC-specific rules.

The design needed to feel close to UPI in terms of flow and interactions, but still handle new CBDC-specific rules.

Key iterations

Key iterations

Reducing visual noise

Reducing visual noise

Reducing visual noise

Initially, we placed multiple UPI actions on one screen, but it caused visual noise.

Initially, we placed multiple UPI actions on one screen, but it caused visual noise.

Initially, we placed multiple UPI actions on one screen, but it caused visual noise.

Split design for clarity

Split design for clarity

Split design for clarity

We shifted to a tabbed approach for better clarity and focus.

We shifted to a tabbed approach for better clarity and focus.

We shifted to a tabbed approach for better clarity and focus.

Data-driven refinements

Data-driven refinements

Data-driven refinements

Post-launch, we reviewed analytics to make final tweaks like reorganizing quick links and improving visibility for masked balance.

Post-launch, we reviewed analytics to make final tweaks like reorganizing quick links and improving visibility for masked balance.

Why this works

Why this works

"Most users open a UPI app to scan a QR and pay quickly — so we made it the first thing they see. This approach turned a 5-step journey into 2."

"Most users open a UPI app to scan a QR and pay quickly — so we made it the first thing they see. This approach turned a 5-step journey into 2."

By removing friction and putting intent-based design first, we helped Kotak’s app feel faster, smarter, and more aligned with how people actually use it.

By removing friction and putting intent-based design first, we helped Kotak’s app feel faster, smarter, and more aligned with how people actually use it.

Project status

Project status

The project is currently in the development phase. The design has been finalized and handed off to the product and engineering teams. Internally, the approach of keeping flows consistent and placing e₹ inside the Wallet section was well-received. The structure is now ready for future testing and rollout.

The project is currently in the development phase. The design has been finalized and handed off to the product and engineering teams. Internally, the approach of keeping flows consistent and placing e₹ inside the Wallet section was well-received. The structure is now ready for future testing and rollout.

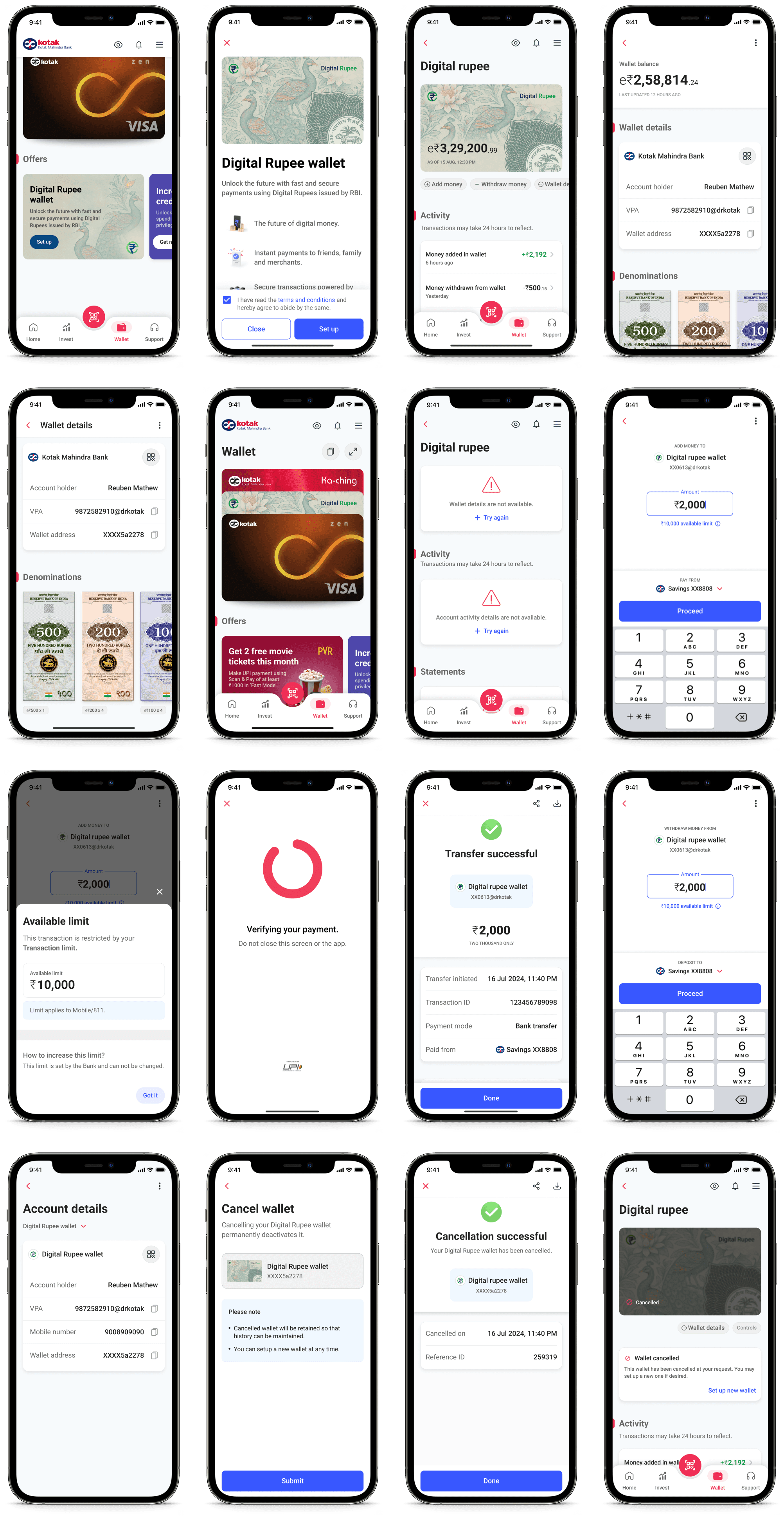

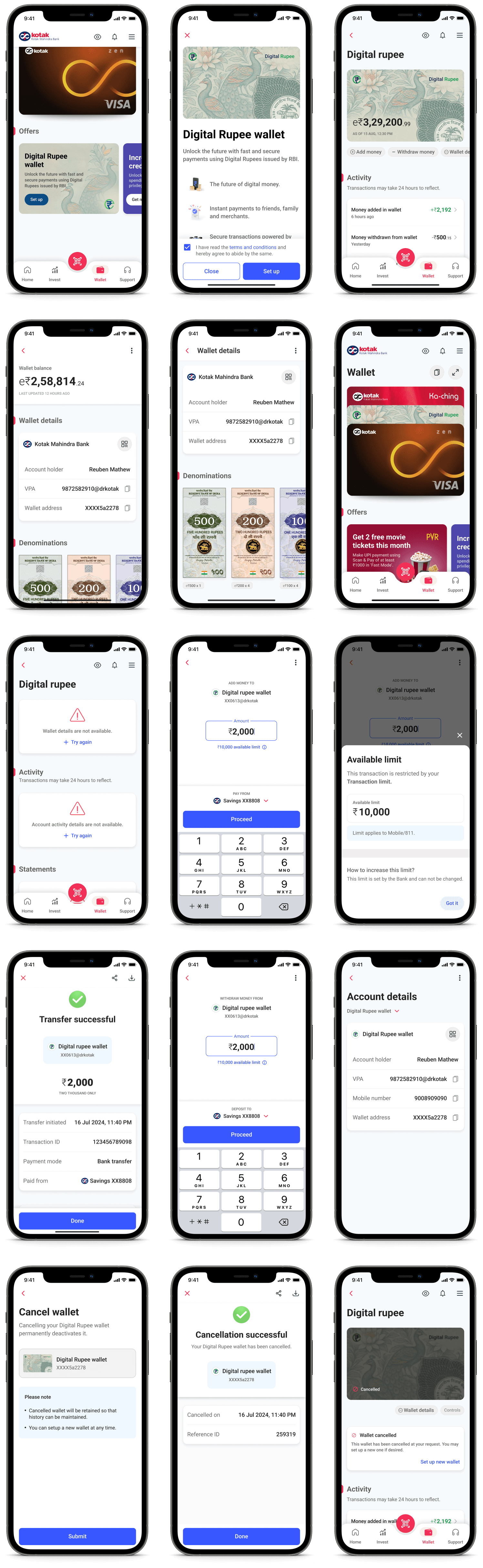

All screens

All screens

Every possible user state was accounted for in the Fast Mode flow — ensuring a smooth experience across different contexts.

Every possible user state was accounted for in the Fast Mode flow — ensuring a smooth experience across different contexts.

Let’s create beautiful

things together.

Let’s create beautiful

things together.

Let’s create beautiful

things together.

Let’s create beautiful

things together.